Will a Balance Transfer Solve Your Credit Card Debt?

What is a Balance Transfer?

A balance transfer is when you move an existing credit card or loan balance to a different credit card account to pay it off. If you have a high balance on one or several credit cards, you can transfer a certain amount up to the credit limit of the new credit card account.

Why You Should Consider a Balance Transfer

Lower interest rates. If you have a high balance on one or more credit cards that both have high-interest rates, you are paying an outrageous amount in interest charges. Plus, if you are only paying the minimum each month, it’s hard to make any headway toward paying down each balance. Transfer a certain amount to a credit card with 0% interest, which will probably only be for a certain amount of time, and start making payments. Your payments will make a bigger dent in paying down debt. Whatever amount you may have left on your initial credit cards will not accrue as much in interest charges.

Simplify the payment process. It can be difficult to keep up with all of your payments, balances and account information for multiple credit accounts. If you are able to, consolidating these balances on one 0% interest credit card can help you monitor your finances. As an added bonus, you’ll only have one payment for the accounts you consolidate.

Chip away at your debt. It can be discouraging when you feel as though you are getting nowhere with your debt. Just think about when you hit the gym for a few weeks, and have no progress to show for it. You wonder if it’s even worth it to keep going. If you dig in and keep at it, though, all the hard work will begin to pay off. It’s like this with paying down your debt. The mental aspect of handling debt is a big part of the picture. Transferring your balance can help you become focused and have a feeling of accomplishment each month.

The Facts About Balance Transfers

You will be paying fees. This should come as no surprise. You are, in fact, dealing with credit cards. Some offer lower fees than others on balance transfers. So make sure you do your homework before applying for a balance transfer credit card. The fee will be a certain percentage of the total amount you transfer. In most cases you will see a 3 percent transfer fee — so if you transfer $5,000 you’ll pay a $150 fee. It might seem a little steep, but if you’re using a card with 0% interest, it could be worth it.

The old bait and switch. Credit card companies are able to lure consumers who are battling debt with the low-interest rate. A 0% interest rate looks too good to be true; how could you pass that up, especially when you have been paying so much interest for so long? The 0% interest rate will not last forever. Normally it will be for six to twelve months. Once this period is over the interest will increase to a normal rate. Unless you pay this balance off before the 0% interest rate expires, you will find yourself in the same situation as before.

New purchases can hurt you. Your new credit card might offer 0% interest on your balance transfer, but may not when it comes to new purchases. Each time you make a purchase on your new credit card you could be paying the normal interest rate charge.

Crunching the Balance Transfer Numbers

We decided to crunch the numbers to show how a balance transfer could help with debt and paying off your credit cards. We decided to use the Balance Transfer Calculator from CreditCards.com to assist in this experiment, which can come in handy when dealing with balance transfers.

The Credit Cards

Breaking down the credit cards:

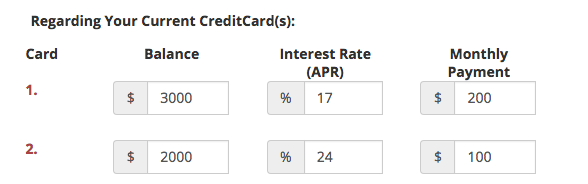

- Credit Card 1

- Balance- $3000

- APR- 17%

- Minimum Payment- $200

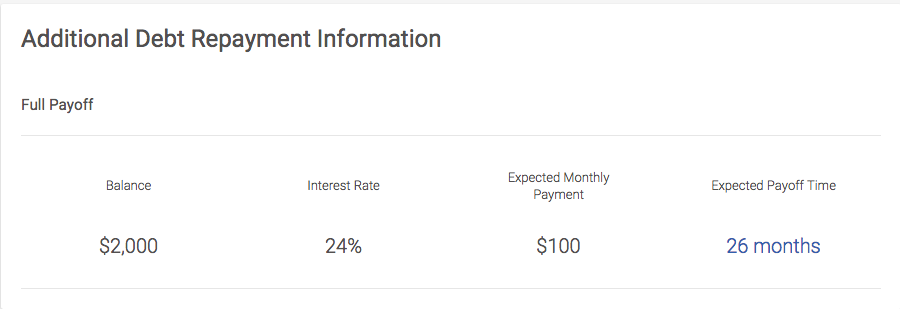

- Credit Card 2

- Balance- $2000

- APR- 24%

- Minimum Payment- $100

So, we went with a total amount of $5,000 because the average household has a little over five thousand in credit card debt.

Each Card by Themselves

We used the CreditKarma.com Debt Pay Off Calculator to help determine how much it would take to pay off each card separately.

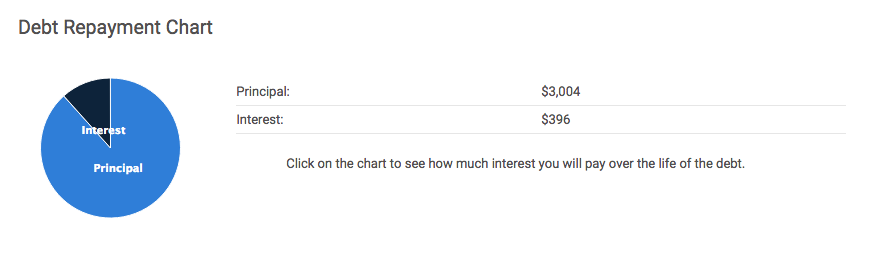

For card number 1, here is how long it would take:

It would take around 17 months to completely pay off this credit card.

You would pay $396 in interest until this credit card is completely paid off.

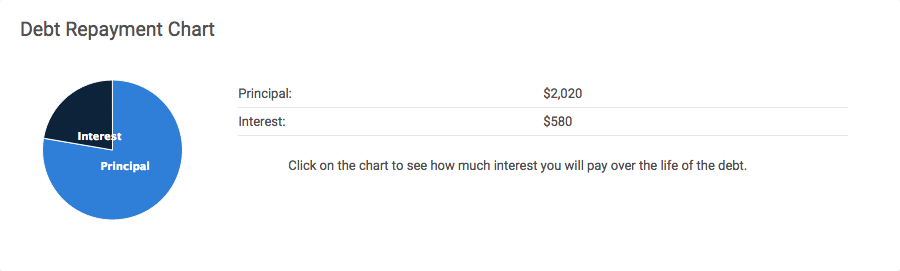

For credit card number 2, here is how long it would take:

It would take you around 26 months to pay this card off completely.

You would pay $580 in interest until this credit card is completely paid off.

Now Let’s Transfer the Balance to One Card

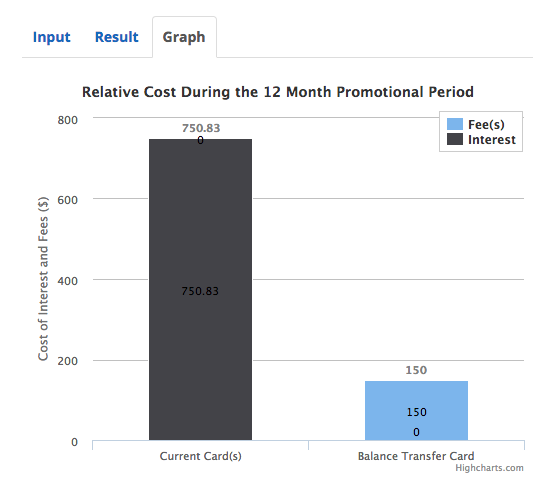

We put in both credit cards including the balance, APR and monthly payment.

Our balance transfer credit card as an introductory APR of zero, and a balance transfer fee of 3%. Meaning, if we transfer the whole balance ($5,000), which will be $150.

The result?

By combining the balances and the monthly payment, you will take 17 months to pay off both credit cards saving $774.45. But, if you were to pin your ears back and pay off the credit card within the 12 month period, you would save a ton of cash.

How a Balance Transfer Affects Your Credit

Your score will drop. When you open a new credit card account, it is assumed that you will be taking on new debt. Applying for a new credit card means that an inquiry will be put on your credit report. New inquiries account for 10% of your credit score. A hit on your report means your score will drop. It’s only a few points, but it does some damage.

The age of your credit will become lower. Credit age is also a factor in determining your credit score, so the older your credit history, the better. A new account will lower the age of all your accounts.

You could help your utilization percentage. Your utilization is determined by your balance compared to available credit. Your limit-to-balance ratio is 30 percent of your credit score. This means it could actually help your credit after a certain amount of time.

What to Remember When Considering a Balance Transfer:

Make sure you know the terms and conditions. Read all the fine print to determine the following:

- The time frame 0% interest is offered.

- What the interest rate will increase to after 0% ends.

- What happens if you make new purchases with the card.

- The transfer fee.

Not knowing this important information could cause you to end up in a worse situation than before.

Will opening a new credit card be worth it? If you have a low credit score you might not qualify for a card that offers 0% interest on balance transfers. It is actually a little more difficult to come across one that will provide this offer if you don’t have at least “good” credit. Make sure that a balance transfer is actually worth it. You might just need to make adjustments to how you manage your finances.

Be absolutely sure you can make the payments. Missing a payment happens. No one is perfect. But if you miss a payment after you have made a balance transfer, your 0% interest offer will probably end.

You’re only going to use the card for a balance transfer. When opening a new card for a balance transfer, you only want to use that card for its original purpose. If you are going to use the card for new purchases, you will be back to paying interest.

Share this story on FlipBoard: Add to Flipboard Magazine.

Want more great financial advice from Robert Palmer? Then be sure to sign-up for the Saving Thousands Newsletter:

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}